DOWNLOAD

DOWNLOAD

August and September 2023 global currencies recap: Dollar Comeback

The US dollar continues to lead the currency pack. But for how long?

By EA Aguirre

By EA Aguirre

After building momentum towards the end of July, the US dollar leveraged this strength to stage a comeback in August.

Early in the month, Fitch Ratings downgraded the US government from AAA to AA+, citing a loss of confidence after lawmakers negotiated up until the last minute on the debt ceiling deal.

This was followed by Moody’s downgrading the credit ratings of several small to medium-sized US banks on concerns surrounding profitability, internal capital, and exposure to underperforming commercial real estate. The headlines ironically supported the demand for dollars as global investors looked for safe haven assets.

On the macroeconomic data front, July non-farm payrolls (NFP) reported only 187,000 new jobs vs. 200,000 forecast while inflation grew by 3.2% year-on-year in line with expectations. In his speech at the Jackson Hole Symposium, Federal Reserve Chair Jerome Powell reiterated sentiments from previous meetings that the central bank will continue to monitor data and adjust monetary policy accordingly.

The data releases and balanced remarks helped ease the dollar by the end of the month but the currency’s accumulated gains were more than enough to cushion these losses.

A weak Japanese yen

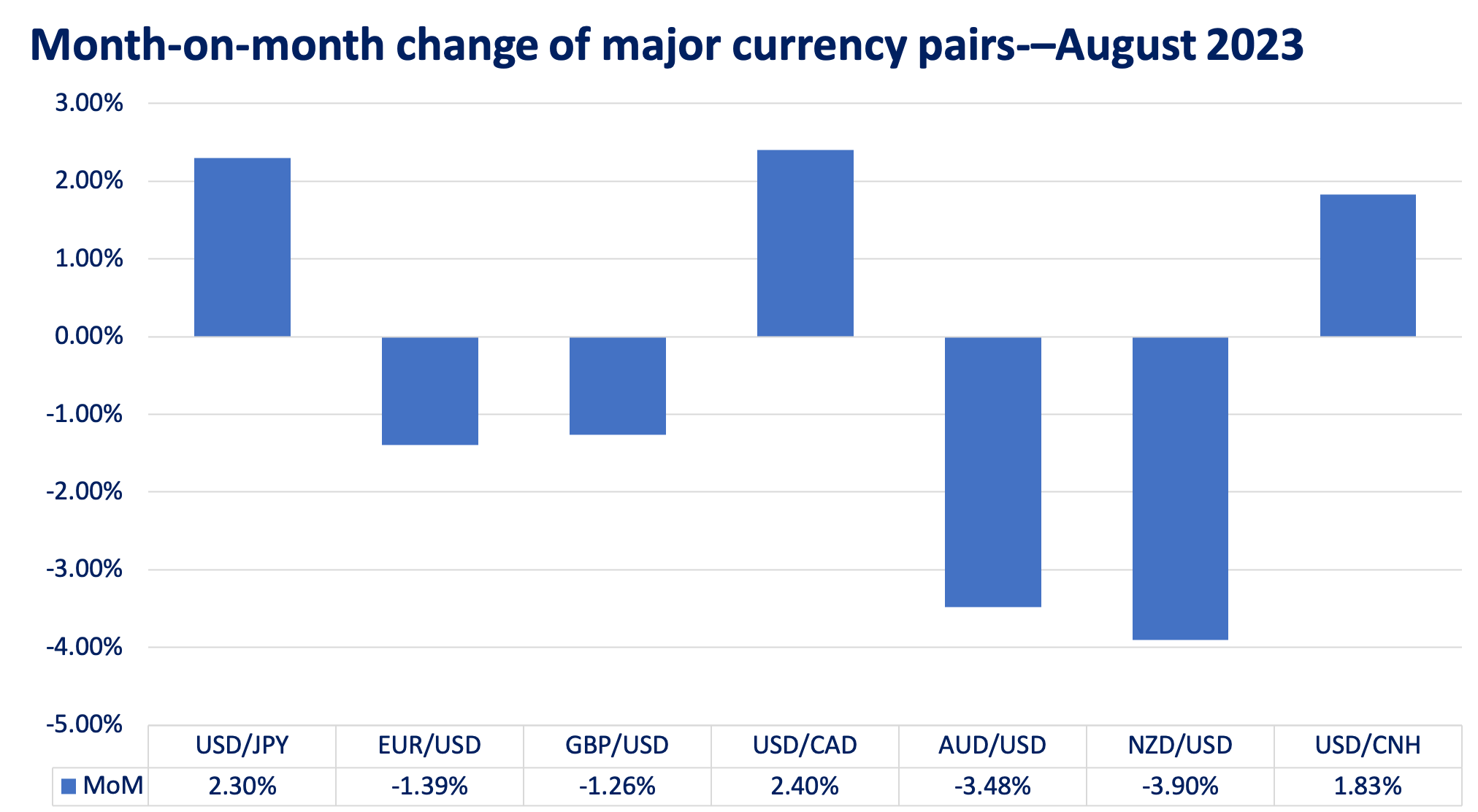

Despite the normally safe haven status of the Japanese yen (JPY), the currency took a beating in August, starting at 143.34, posting a new year-to-date high of 147.32, and then returning to 145.54 (+2.30%). Finance Minister Shunichi Suzuki expressed that his team was monitoring the foreign exchange market with a “high sense of urgency” but this did little to prevent the yen’s weakness.

Meanwhile, Bank of Japan (BOJ) Governor Kazuo Ueda continued to defend the ultra-loose monetary policy, stating that even as headline inflation remained above 3%, wages have to grow by more than 2% before he can consider policy normalization. Given renewed dollar strength, our foreign exchange traders expect USD/JPY to continue rising but are wary of the possibility of intervention, which Japanese regulators have done before.

Pessimistic outlook affects euro

The euro (EUR) dropped 1.40% from 1.0984 to 1.0843 on dollar strength as well as disappointing economic data within the Eurozone. The composite purchasing managers’ index (PMI), a measure of manufacturing and services activity compiled by S&P Global, dropped to a score of 47 in August vs. 48.5 forecast and 48.6 in July. This was well below the 50-mark separating growth from contraction as high interest rates discourage business activity, with Germany experiencing the steepest decline.

Even after July inflation printed slightly higher at 5.3% year-on-year vs. 5.1% forecast, the EUR/USD struggled to go higher. On September 14, the European Central Bank (ECB) unexpectedly hiked rates by 25 basis points (bps) but then signaled that it may already be done with its tightening cycle. Pessimistic outlook remains on the horizon for the currency as lackluster domestic data and persistent inflationary risks could translate to potential stagflation.

Brakes applied on GBP and AUD; CAD makes gains

After posting two consecutive months of gains, the pound sterling (GBP) lost its momentum against the US dollar, falling by 1.26% from 1.2777 to 1.2673. Despite the Bank of England (BOE) hiking policy rates by 25 bps to 5.25%, investors pulled back their bullish GBP bets after it was revealed that the vote was split with the minority preferring a 50-bp hike.

Throughout the month, the GBP found some support from June wages increasing by 8.2% year-on-year vs. 7.3% forecast and July inflation printing 6.8% year-on-year as expected. However, the currency was let down by a contractionary August composite PMI score of 48.6, a higher unemployment rate of 4.2%, and a decline in retail sales of 1.2% month-on-month. In its September meeting, the BOE decided to pause rates at 5.25% in a tight 5-4 vote, but will likely leave rates higher for longer, which could still help support the GBP amid a stronger dollar.

Commodity-linked currencies lost the most in the Group-of-10 space. The Canadian dollar (CAD) ended the month higher by 2.41% from 1.3281 to 1.3508. Despite inflation rebounding to 3.3% year-on-year in July from 2.8% in June, it seems that the Bank of Canada (BOC) may already be done with its tightening cycle.

Markets also paid more attention to weakness in Canada’s labor market with employment dropping by 6,400 instead of an expected gain of 21,100. There is still some hope for the CAD as higher oil prices brought about by extended supply cuts from Saudi Arabia and Russia should boost Canada’s oil revenues.

The Reserve Banks of Australia (RBA) and New Zealand (RBNZ) continued to leave policy interest rates unchanged at 4.10% and 5.50% respectively. To make matters worse for the RBA, markets actually expected a 25-bp hike after second quarter inflation printed at 6%, still well above the central bank’s 2% target.

The Australian dollar (AUD) fell from 0.6613 to 0.6484 (-3.48%). Domestic data also missed estimates and brought weakness to the local currency. Wage growth was lower-than-expected at 3.6% year-on-year in June vs. 3.7% forecast. The unemployment rate increased to 3.7% in July from 3.5% the previous month due to growth in labor participation.

The New Zealand dollar (NZD) was the biggest loser in August, dropping from 0.6149 to 0.5967 (-3.90%). Similar to its neighbor, New Zealand’s unemployment rate increased to 3.6% from 3.4% in the first quarter on increased labor participation.

The sell-off in NZD was exacerbated when the country’s manufacturing index dropped to a score of 46.2 vs. 49.4 forecast. With RBA and RBNZ seemingly done with their tightening cycles, the AUD and NZD will likely see continued weakness against the US dollar until their countries start to see sustained economic growth.

CNH loses ground

The Offshore Chinese yuan (CNH) lost gains made in July with USD/CNH rising 1.83% from 7.1856 to 7.2755 but not before hitting intra-month highs at the 7.3496. The currency started the month on the back foot with its own Manufacturing PMI printing worse than expected at 49.2 compared to scores above 50 over the last two months.

A series of disappointing data pointing to weaker economic growth followed, particularly new yuan banks loans which declined by a staggering 89% from 3.05 trillion yuan in June to 345.9 billion yuan in July. The People’s Bank of China (PBOC) rushed to cut its medium-term lending facility rate by 15 bps and its 7-day reverse repurchase rate by 10 bps. It also ordered local banks to step up intervention in supporting the yuan.

The last few days of August saw some headlines on Chinese authorities committing to support the struggling property market, but the lack of concrete details kept USD/CNH elevated. The desk remains biased towards a weaker yuan but expects intervention from authorities should the currency pair return to the 7.33 to 7.35-level once more.

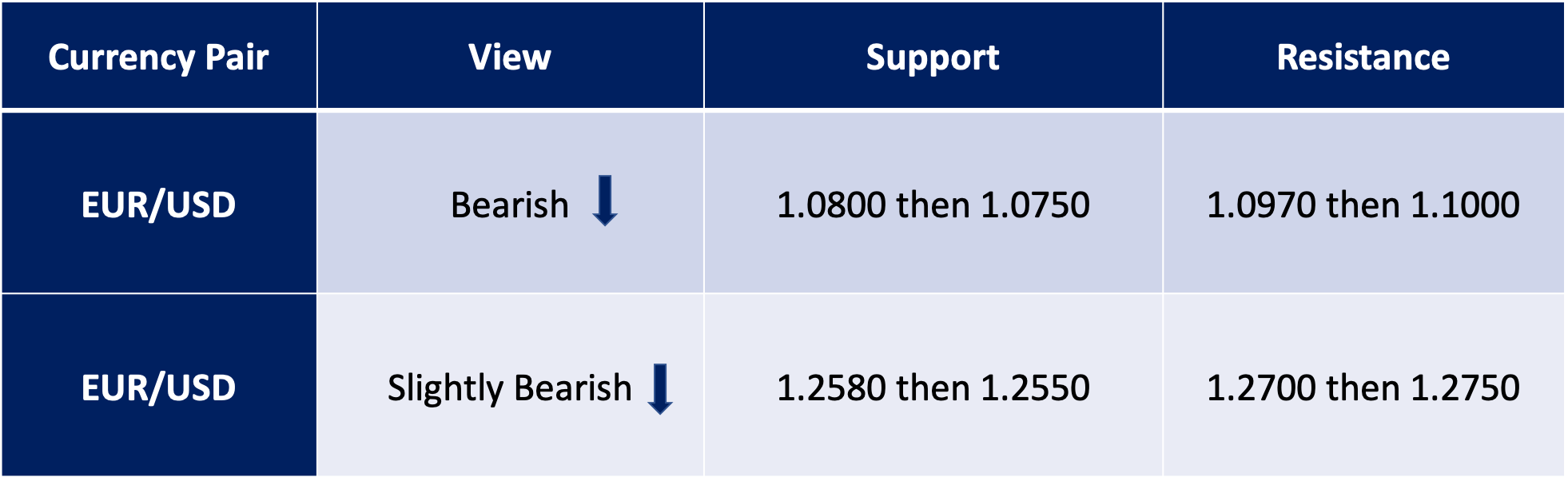

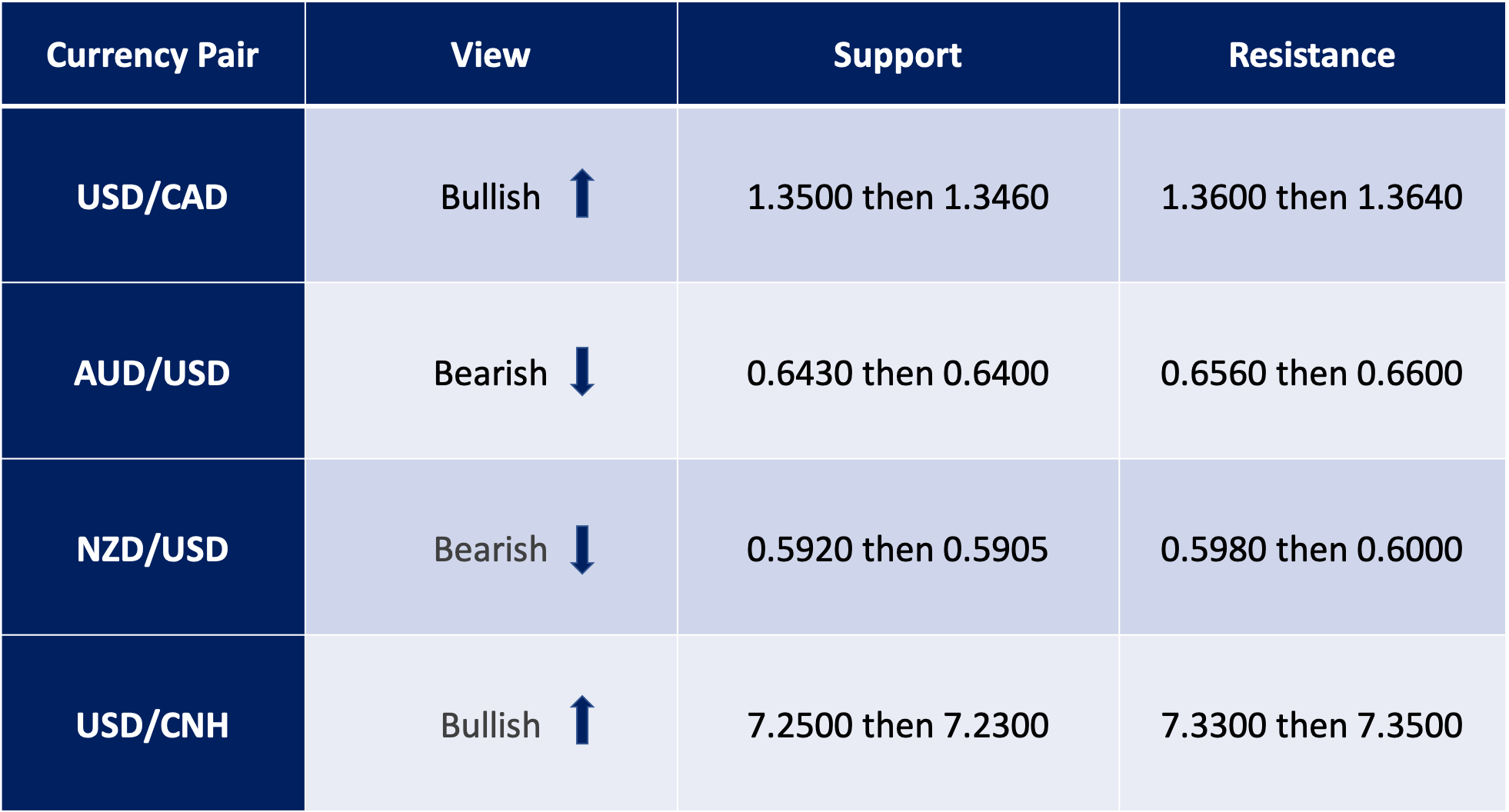

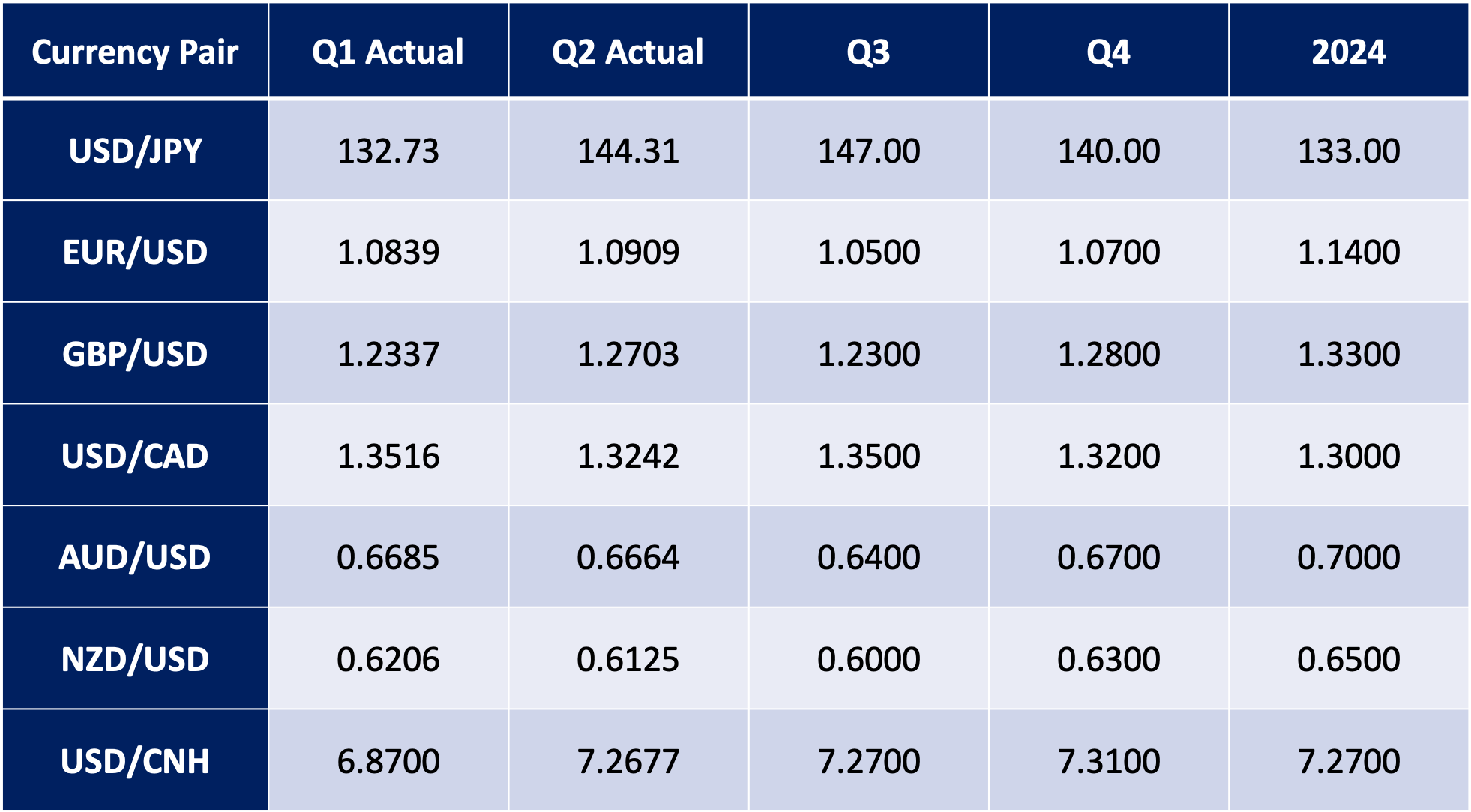

FX Traders’ Forecasts

The above forecasts are the foreign exchange traders’ personal opinions and may not reflect the official views of the bank.

The month of August has proven that despite concerns over weakness in the US political and financial systems, the US dollar and US treasury securities will continue to be the preferred safe-haven assets of global investors. In an environment of rebounding inflation due to rising energy and food prices, the US continues to outlast its peers, whose economies are already feeling the brunt of elevated interest rates.

Markets will be focusing on every US economic data release until the end of the year to determine whether the US economy can truly stomach one more policy rate hike.

EARL ANDREW “EA” AGUIRRE is a Market Strategist at Metrobank’s Financial Markets Sector and has 10 years of experience in foreign exchange, fixed income securities, and derivatives sales. He has a Master’s in Business Administration from the Ateneo Graduate School of Business. His interests include regularly traveling to Japan and learning its language and culture.