DOWNLOAD

DOWNLOAD

Ask Your Advisor: Should I take profit on long-dated government securities?

There is a right time to take profit and reinvest your funds depending on your goals and situation.

By Earl Andrew A. Aguirre

By Earl Andrew A. Aguirre

Over the last two years, we recommended that peso government securities (GS) investors buy 5- to 20-year bonds paying coupons of at least 5% per annum (p.a.) net in order to position for lower interest rates.

Now that both the US Federal Reserve (Fed) and Bangko Sentral ng Pilipinas (BSP) have started cutting rates, investors who followed our advice should already start to see significant unrealized gains on their long-dated GS.

Lauren (not her real name), a 75-year-old client living off her pension and investments, is one of them. And she has a question: Should I start taking profit by selling these bonds? And where should I reinvest the proceeds?

Over the years, she has amassed a portfolio of over PHP 100 million in peso government and corporate bonds. Among these are PHP 30 million in 7- to 20-year bonds that have already paid a number of coupon interest payouts and are also trading well above their original purchase price or in-the-money.

What’s interesting about Lauren is that she is also an avid bond trader herself. When she sees unrealized gains in her portfolio, she wants to lock in the profits and look for new bonds to enter into. Lauren asked us what to do.

We presented some scenarios.

1. Hold To Maturity (HTM)

On one hand, Lauren will continue to benefit from relatively high coupon interest paid by these bonds. Rising domestic inflation during the COVID-19 pandemic resulted in the BSP aggressively hiking its policy interest rates, allowing the Bureau of the Treasury (BTr) to issue government debt at record high coupon rates. Her in-the-money bonds include:

| Security Name | Gross Coupon Rate | Maturity Date |

|---|---|---|

| FXTN 10-70 | 7.500% | 20 Oct 2032 |

| FXTN 25-5 | 8.500% | 29 Nov 2032 |

| FXTN 10-72 | 6.250% | 25 Jan 2034 |

| FXTN 25-8 | 8.125% | 16 Dec 2035 |

| FXTN 15-1 | 7.000% | 13 Jul 2038 |

| FXTN 20-23 | 6.750% | 24 Jan 2039 |

| FXTN 20-25 | 8.125% | 24 Nov 2042 |

| FXTN 20-27 | 6.875% | 23 May 2044 |

After 20% withholding tax, she is expected to receive an average net coupon of 5.4% per annum over an average remaining tenor of 12 years. Lauren can simply live off the passive income as interest rates ease back to their pre-pandemic normal. This can greatly supplement her pension and other investments. On the other hand, this could also mean foregoing potential profits from trading these in-the-money bonds in the secondary market.

2. Switch to the front to belly of the curve

These are not her only investments generating passive income, just the ones that will result in trading gains. If she sells these in-the-money bonds, she is estimated to generate up to PHP 5 million in profits or roughly 8% per annum over the last one and a half years of holding these bonds.

When proposing where to reinvest the sales proceeds, we factored in her age as well as current economic conditions affecting the GS market. Although she benefits from recurring interest income, as a 75-year-old, it is advisable that Lauren doesn’t extend her investment duration too long so that she can remain liquid in the event of emergencies.

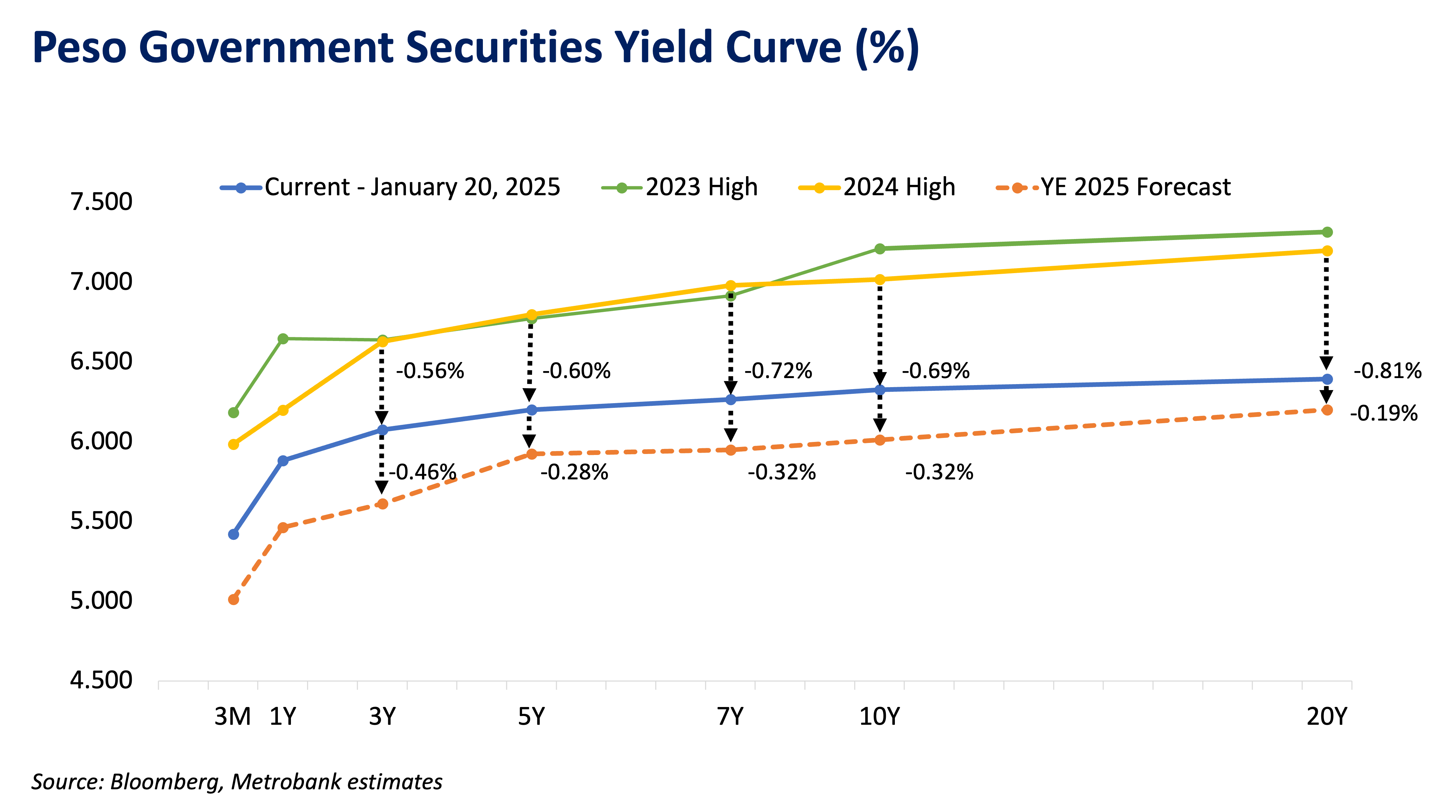

Now let’s turn to what’s happening in the GS market. Plotting down the yields of various bonds across different maturity dates results in the GS yield curve. The chart below shows that the yield curve has flattened considerably from the highs seen in 2023 and 2024. Much of this is due to the strong demand for high-coupon long-dated bonds leading up to the inevitable rate cuts by the BSP.

Source: Bloomberg, Metrobank Local Currency Trading Department estimates

While our fixed income traders expect the yield curve to keep falling by the end of 2025, they believe that its shape will be much steeper, meaning that yields at the front to belly of the curve (1 to 5 years) will fall much more than the back end (7 to 20 years).

There are two reasons for this shape:

- The front and belly are more sensitive to rate cuts by the BSP, which will continue to happen as inflation settles in the central bank’s 2-4% target range.

- Long-dated GS are expected to mirror rising yields in the US Treasuries market. US President Trump’s proposed policies of tax cuts on corporations and the rich are expected to be funded through the issuance of 10-year and 30-year US Treasury bonds, which may put upward pressure on long-term rates and spillover to the GS market.

Synthesizing these different views, we recommended to Lauren that she sell her in-the-money 7- to 20-year bonds to lock in that PHP 5 million profit and then reinvest the proceeds in our preferred 1- to 5-year GS:

| Security Name | Gross Coupon Rate | Maturity Date | Indicative Gross Yield To Maturity (YTM) as of 20 Jan 2025 |

|---|---|---|---|

| TBILL 07.16.25 | N/A | 16 Jul 2025 | 5.550% |

| RTB 5-13 | 2.625% | 20 Sep 2026 | 5.715% |

| RTB 5-15 | 4.875% | 4 Mar 2027 | 5.910% |

| RTB 5-17 | 6.125% | 22 Aug 2028 | 6.100% |

| RTB 5-18 | 6.250% | 28 Feb 2029 | 6.145% |

Switching to these bonds will reduce her average net coupon to 4.7% per annum from the 5.4% per annum that she currently enjoys. However, if our view of a steeper yield curve is correct, then these shorter-dated bonds should see additional capital gains from lower market yields.

Lauren may then choose to hold these new bonds to maturity or trade them and reposition in longer-dated bonds again once yields in the back end improve.

Trading GS and other bonds can be a way to generate returns beyond the coupons that the securities commit to pay. However, these strategies are more appropriate for moderate and aggressive clients who can tolerate potential losses if the trade idea does not pan out.

Conservative clients who prioritize capital preservation are encouraged to hold their securities to maturity to fully realize the indicative returns provided.

To view daily indicative yields of these specific government securities and look through our other bond offerings, you may log-in to Metrobank Wealth Manager or reach out to your investment specialist.

(Disclaimer: This is general investment information only and does not constitute an offer or guarantee, with all investment decisions made at your own risk. The bank takes no responsibility for any potential losses. You may consult your relationship manager or investment specialist for proper investment advice. Not a client yet? Please sign up here so you can begin your wealth journey with us.)

EARL ANDREW “EA” AGUIRRE is the Head of the Investment Counselor Department under the Financial Markets Sector of Metrobank. He has over 10 years of experience in foreign exchange, fixed income securities, and derivatives sales. He has a Master’s in Business Administration from the Ateneo Graduate School of Business. His interests include regularly traveling to Japan and learning its language and culture.