DOWNLOAD

DOWNLOAD

Forecast Update: Inflation paths, rate cuts, and the dollar’s U-turn

The tariff war sent shock waves across global markets. Here are our forecasts and the trends we see.

By Metrobank

By Metrobank

With tariffs and counter tariffs continuing to stir markets, investors wonder about the repercussions.

Here is what we think will happen:

Philippine inflation will cool.

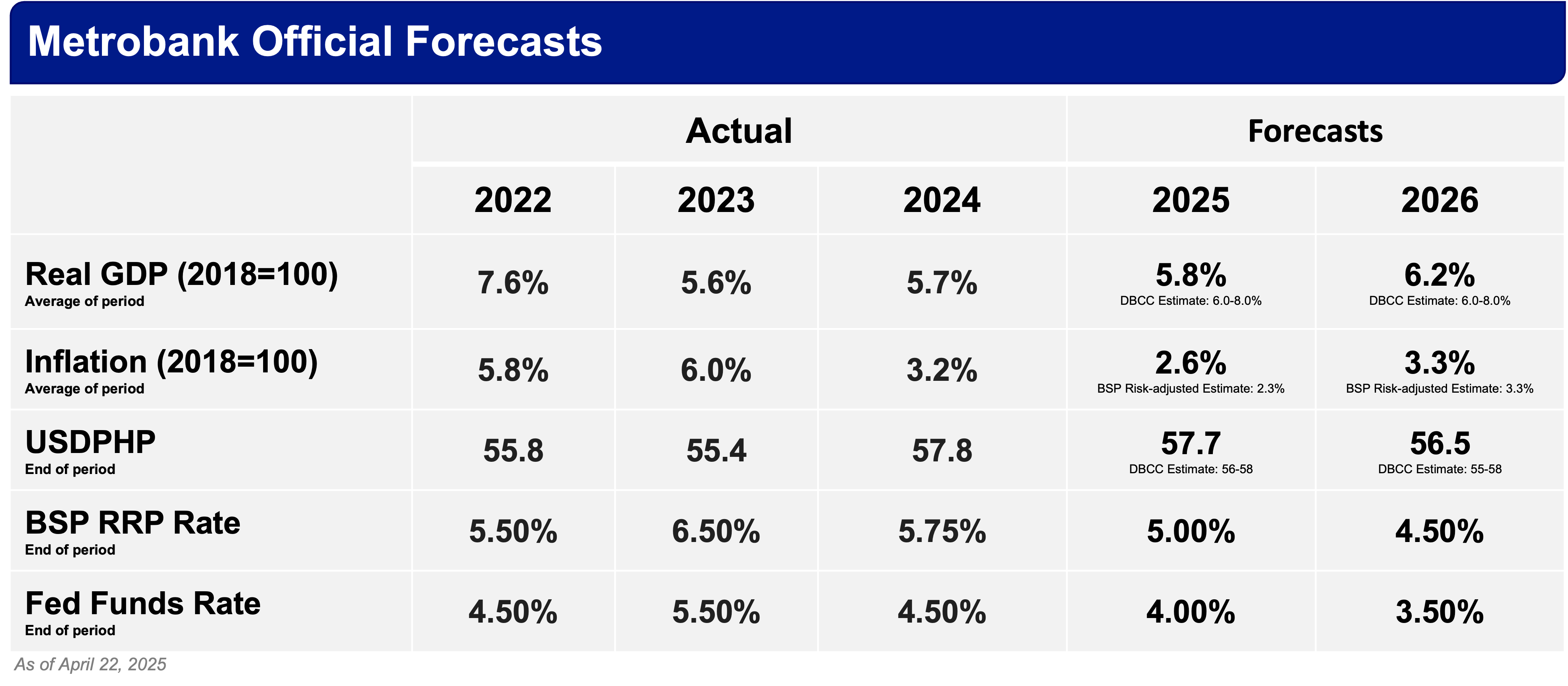

We have revised our 2025 full-year average inflation forecast to 2.6% from the previous 3.0% due to the downward pressure exerted by food commodities and global oil prices. Lower oil prices are driven by weak global demand due to a bleak global economic outlook.

US President Donald Trump’s blanket tariffs remain an upside risk to inflation. However, the 90-day reprieve on the implementation of the higher tariffs on some countries, including the 17% for the Philippines, provides space for negotiation with the US to lower the top-up tariff.

Nonetheless, these blanket tariffs could still contribute a pass-through effect on domestic prices, as rising global prices could potentially seep into the local economy. Within-target inflation is expected to persist until next year but potentially settling higher at 3.3%.

This slight upward revision from Metrobank’s previous forecast of 3.2% for 2026 accounts for base effects as well as expectations for imported inflation due to higher global commodity prices.

Higher US inflation will cap Fed rate cuts.

A higher risk of a recession in the US provides urgency for the US Fed to continue easing monetary conditions despite elevated inflation and the risk of a weaker labor market. With this, we maintain our year-end forecast of 4.00% for the federal funds rate (FFR).

However, as the tariff war instigated by the US against the rest of the world continues to escalate, the cost of imported inflation is expected to increase, providing a cap for rate cuts by the Fed. Given this, we have revised our end-2026 FFR forecast to 3.50%.

This translates to a cumulative 50 basis points (bps) worth of cuts each for 2025 and 2026.

The BSP will cut deeper than the Fed.

The Bangko Sentral ng Pilipinas (BSP) revised its 2025 risk-adjusted forecast lower to 2.3% from 3.5% previously. Recent statements from BSP Governor Eli Remolona Jr. also signaled a potential move to adjust the target range lower to 1.5%-3.5% from 2.0%-4.0%.

Contrary to an outlook of higher inflation compared to the rest of the world, the Philippines’ inflation outlook is likely to remain consistent with the current 2.0%-4.0% target. This leaves enough cushion to absorb any potential upside risks related to higher global commodity prices emerging from the trade war between the US and the rest of the world.

Moreover, weaker global demand as the world anticipates a global slowdown will lead to a wider trade deficit. This will provide more urgency for the BSP to deliver more cuts this year to support the domestic economy.

Lastly, the current dollar-peso exchange level amid the dollar’s weakness signals the capacity for the peso to maintain the current 100-bp interest rate differential (IRD) with the Fed.

With this, we have revised our year-end reverse repurchase (RRP) rate forecast to 5.00% from 5.25% previously. However, the end-2026 forecast for the RRP is maintained at 4.50%. This translates to a cumulative 75 bps and 50 bps worth of cuts in 2025 and 2026, respectively.

The US dollar will take a U-turn down tariff road.

After rallying in the latter part of last year, we have now seen the US dollar take a U-turn amid concerns about softer US growth. US President Donald Trump’s tariff war is expected to continue once the 90-day reprieve ends.

Now markets are worried. With greater inflationary pressure on the horizon for the US, concern over economic growth takes center stage and markets are now pricing in more Fed cuts.

We have revised our year-end forecast for the USD/PHP to 57.7 from the previous 57.9, considering recent dollar near-term weakness coupled with expectations of a reversal later in the year due to renewed seasonal demand for the US dollar in 3Q 2025.

(Disclaimer: This is general investment information only and does not constitute an offer or guarantee, with all investment decisions made at your own risk. The bank takes no responsibility for any potential losses.)