DOWNLOAD

DOWNLOAD

Peso GS Weekly: Local yield curve steepens post-BSP rate cut

Offshore players began to unload at the belly and back-end of the curve as the dollar remains resilient. Meanwhile, others load up on short-term securities due to scarce supply.

By Metrobank Local Currency Trading Department and Maria Christina Virtudazo

By Metrobank Local Currency Trading Department and Maria Christina Virtudazo

WHAT HAPPENED LAST WEEK

The local government securities (GS) market opened weak despite liquidity being freed up by the maturity of the Fixed Rate Treasury Note 5-76, leading to a steepening of the GS curve.

On Oct. 16, the Bangko Sentral ng Pilipinas cut the key overnight rate by 25 basis points (bps), as widely expected. Some knee-jerk selling, however, was seen after the central bank released its updated inflation forecasts. The risk-adjusted inflation forecast for 2025 was adjusted higher to 3.3% from 2.9%, while the 2026 inflation forecast was updated to 3.7% from 3.3%.

With the USD/PHP exchange rate remaining elevated for most of last week, selling interest from offshore participants continued as they unloaded benchmark 5- to 20-Year bonds. Other institutional onshore accounts, however, were bottom fishers of 2- to 4-Year bonds as supply has started to become scarce in this part of the curve.

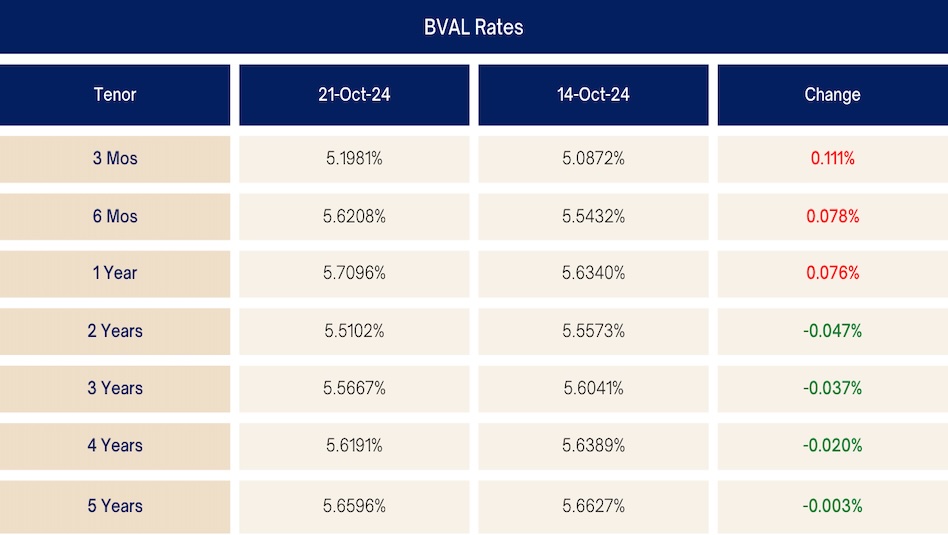

Week-on-week, 4-Year bonds ended lower by as much as 10 bps, while 5- to 20-Year bonds ended marginally changed to 4 bps higher.

Market Levels (week-on-week)

WHAT WE CAN EXPECT

We remain better buyers of medium-term bonds on continued selloffs in anticipation of the additional liquidity to be freed up by the cut in banks’ Reserve Requirement Ratio (RRR) from 9.50% to 7.00%.

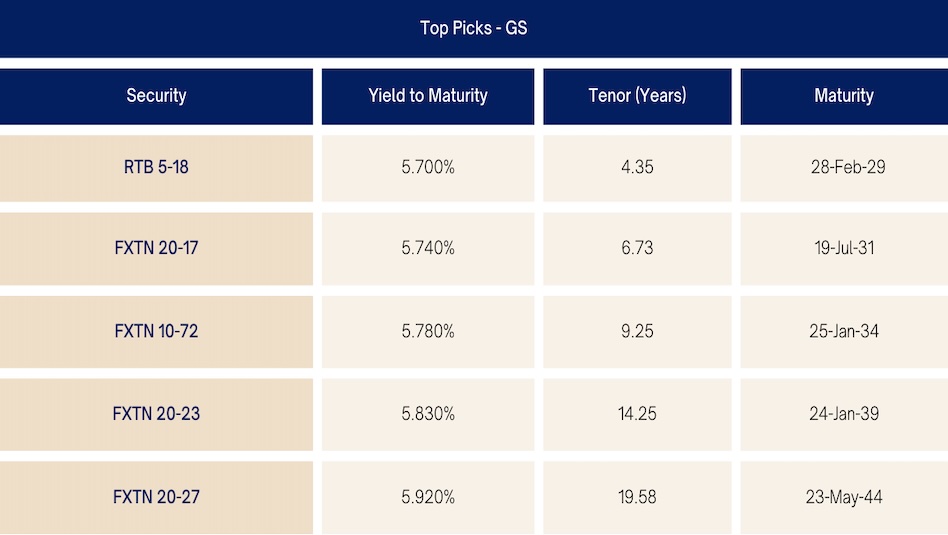

At current levels, we recommend the Retail Treasury Bond 5-18 at 5.675% since the yield premium when extending duration to 7- to 10-Year remains minimal. With just four bond auctions left for the year, we think that yields will remain supported as the additional supply is limited.

Beyond this month’s developments, eyes will be on the much-anticipated US election and its effect on financial markets.

See our top picks below:

Note: Rates are indicative and subject to refresh.