DOWNLOAD

DOWNLOAD

Peso GS Weekly: Local yields continue to rally

The central bank’s 25-bp policy rate cut is driving market activity with better sellers leading the way.

By Metrobank Local Currency Trading Department and Maria Christina Virtudazo

By Metrobank Local Currency Trading Department and Maria Christina Virtudazo

WHAT HAPPENED LAST WEEK

To start the week, price action was initially range-bound with movements more dependent on local factors despite the packed US economic calendar. Even though US Treasury yields closed higher on good economic data, the local government securities (GS) market saw better buying. Market participants also remained split at first on whether the Bangko Sentral ng Pilipinas (BSP) will adjust key policy rates in their August Monetary Board (MB) meeting given the latest hawkish statements of BSP Governor Eli Remolona Jr. after the July Consumer Price Index (CPI) print and 2nd quarter Gross Domestic Product (GDP) results were released.

On Tuesday, the Bureau of the Treasury (BTr) fully awarded the reissuance of the 7-Year Fixed Rate Treasury Note (FXTN) 20-17 at an average of 6.128%, with accepted yields within market indications ranging from 6.05% to 6.14%.

On Thursday, the much-awaited MB meeting saw the BSP cut key rates by 25 basis points (bps), bringing the overnight reverse repurchase rate to 6.25%. Yields across the curve fell immediately after the announcement as those light with inventory chased the move.

To end the week, the price action on Friday was a continuation of the better buying interest, with both dealers and clients driving trading interest. The belly of the curve continued to outperform with 7-Year to 10-Year benchmark bonds printing below 6%.

On a week-on-week basis, bonds rallied by as much as 13 bps with dealers preferring the 10-Year bonds as it will not be reissued anymore for this quarter.

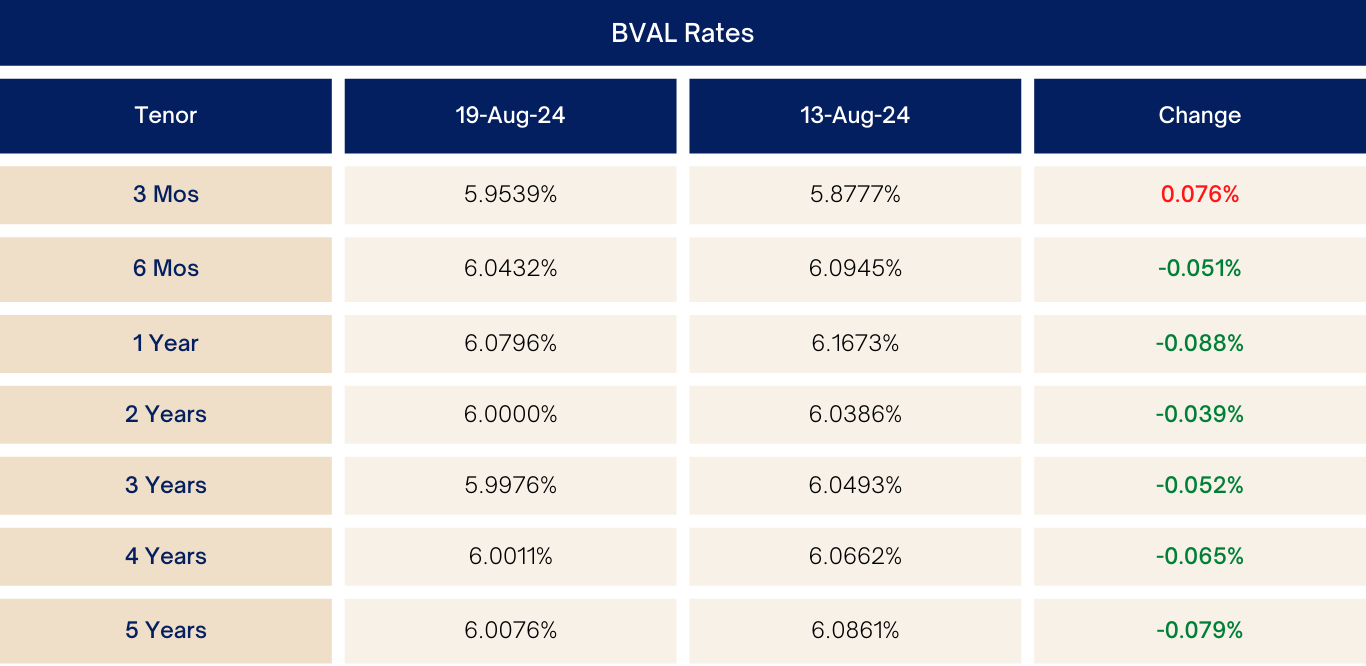

Market Levels (week-on-week)

WHAT WE CAN EXPECT

At current levels, we expect the GS curve to remain supported, with increased activity in short-dated securities such as T-bills and BSP Bills as the market adjusts to the BSP’s rate cut. The Fixed Rate Treasury Note (FXTN) 10-59 maturity today will also influence any dealer selling interest as institutional clients roll their maturity proceeds.

The BTr will reissue the FXTN 20-23 for this week’s 14-Year auction with a target yield range of 6.05-6.15%. Strong participation is expected to be seen in this auction as there will be no issuance on this part of the curve next month, and this auction coincides with the FXTN 10-59 maturity where an estimate of PHP 120 billion worth of funds will be freed up.

See our top picks below:

Note: Rates are indicative and subject to refresh.