DOWNLOAD

DOWNLOAD

Bond Investing: Strike at the belly of the curve

Since the start of the most recent rally, yields of long-dated bonds have fallen faster than yields in the front-end. Where do investors deploy funds in a flat curve like this?

By Metrobank Rates and Credits Department, EA Aguirre, Joshua Tatlonghari, and Yna Virtudazo

By Metrobank Rates and Credits Department, EA Aguirre, Joshua Tatlonghari, and Yna Virtudazo

Over the past few weeks, the government securities (GS) curve has significantly bull flattened on renewed appetite for duration, or the willingness to take on more interest rate risk by purchasing longer-term bonds. Bull flattening occurs when long-term rates fall faster than short-term rates, causing the yield curve to flatten.

Investors were keen to maximize the potential move lower in yields amid possible rate cuts from the Bangko Sentral ng Pilipinas (BSP). This trend is also supported by the rally in global yields after weak data prints from the United States, which can be seen as markets are already pricing in more than four rate cuts for the year. This has translated to aggressive risk-taking in the secondary market that eventually spilled over to the Bureau of the Treasury’s (BTr) auctions.

Strong bidding interest was seen near the lower end of market indications as investors sought to secure awarded volume. Since this rally began in the last week of June, bonds in the back-end of the curve have appreciated by as much as 45 basis points.

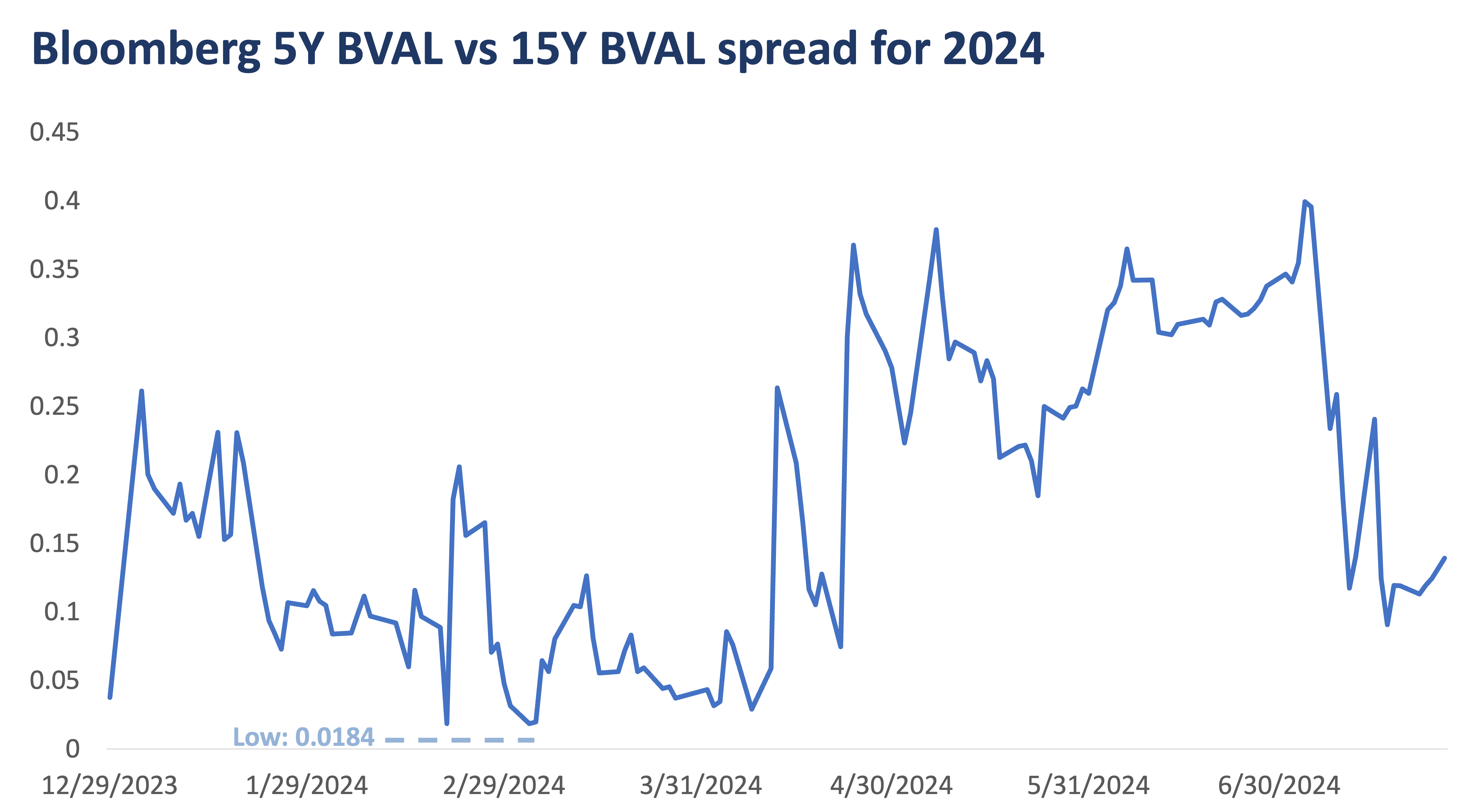

At current levels, we believe that the yield curve is too flat given the magnitude of the rally. Currently, 12-year to 15-year bonds are trading near the 6.080-6.1250% range, while 5-year to 7-year bonds are trading relatively close at 6.050-6.070% — a minimal difference compared to previous levels.

Additionally, the spread between 5-year and 15-year bonds has significantly compressed, narrowing from their widest point this year of 40 basis points (bps) to 14 bps during the first week of July. This compression indicates unusual pricing in the market, as longer-term yields should typically be higher to compensate for greater risk.

Trade Ideas

Given the current circumstances, we believe that longer-dated bonds are most susceptible to underperforming given the possible shift in market sentiment as investors pull back on rate cut expectations and increased volatility in the global bond space leads to a steepening of the yield curve.

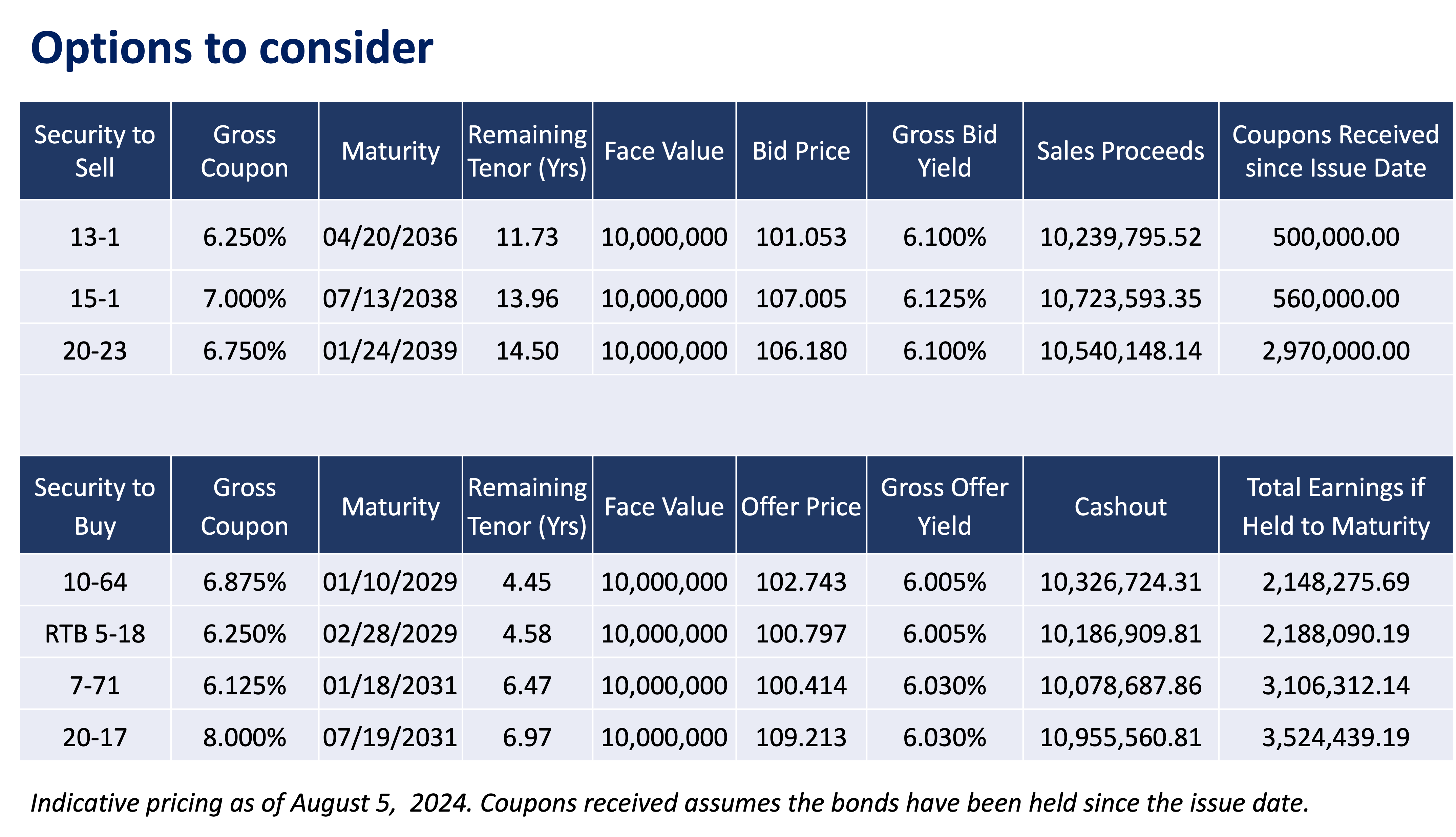

We recommend selling 11-year to 15-year bonds given the flatness mentioned above. Additionally, we suggest remaining patient before heavily reinstating positions in this space and would prefer for the term premium to increase first. The term premium refers to the additional yield investors require for holding longer-term bonds compared to shorter-term bonds.

In terms of relative value, we observe that 5-year to 7-year bonds are the most attractive. This range offers a more favorable risk-return profile, making it an opportune time to invest in these medium-term bonds.

We only recommend clients reinstate their positions in 10-year and 20-year bonds at 6.20% and 6.30%, respectively, through the upcoming BTr auctions.

EARL ANDREW “EA” AGUIRRE is a Market Strategist at Metrobank’s Financial Markets Sector and has 10 years of experience in foreign exchange, fixed income securities, and derivatives sales. He has a Master’s in Business Administration from the Ateneo Graduate School of Business. His interests include regularly traveling to Japan and learning its language and culture.

JOSHUA TATLONGHARI is a Financial Markets Analyst at Metrobank’s Institutional Investor Coverage Division. He holds an undergraduate degree in finance from the University of Santo Tomas and is currently taking a Master’s degree in Applied Economics at De La Salle University-Manila. He spends his free time working out and watching documentary videos relating to finance and the economy.

MARIA CHRISTINA VIRTUDAZO is an Investment Counselor at Metrobank’s Institutional Investor Coverage Division. She graduated with a Bachelor’s degree in Business Administration from the University of the Philippines – Diliman. She spends her free time listening to K-pop, writing fanfiction, and watching Netflix series and K-dramas.