DOWNLOAD

DOWNLOAD

Peso GS Weekly: Significant demand in the belly of the curve

At current levels, take profit at the longer-tenor bonds and shift to bonds in the belly of the curve.

By Metrobank Local Currency Trading Department and Joshua Enrick Tatlonghari

By Metrobank Local Currency Trading Department and Joshua Enrick Tatlonghari

WHAT HAPPENED LAST WEEK

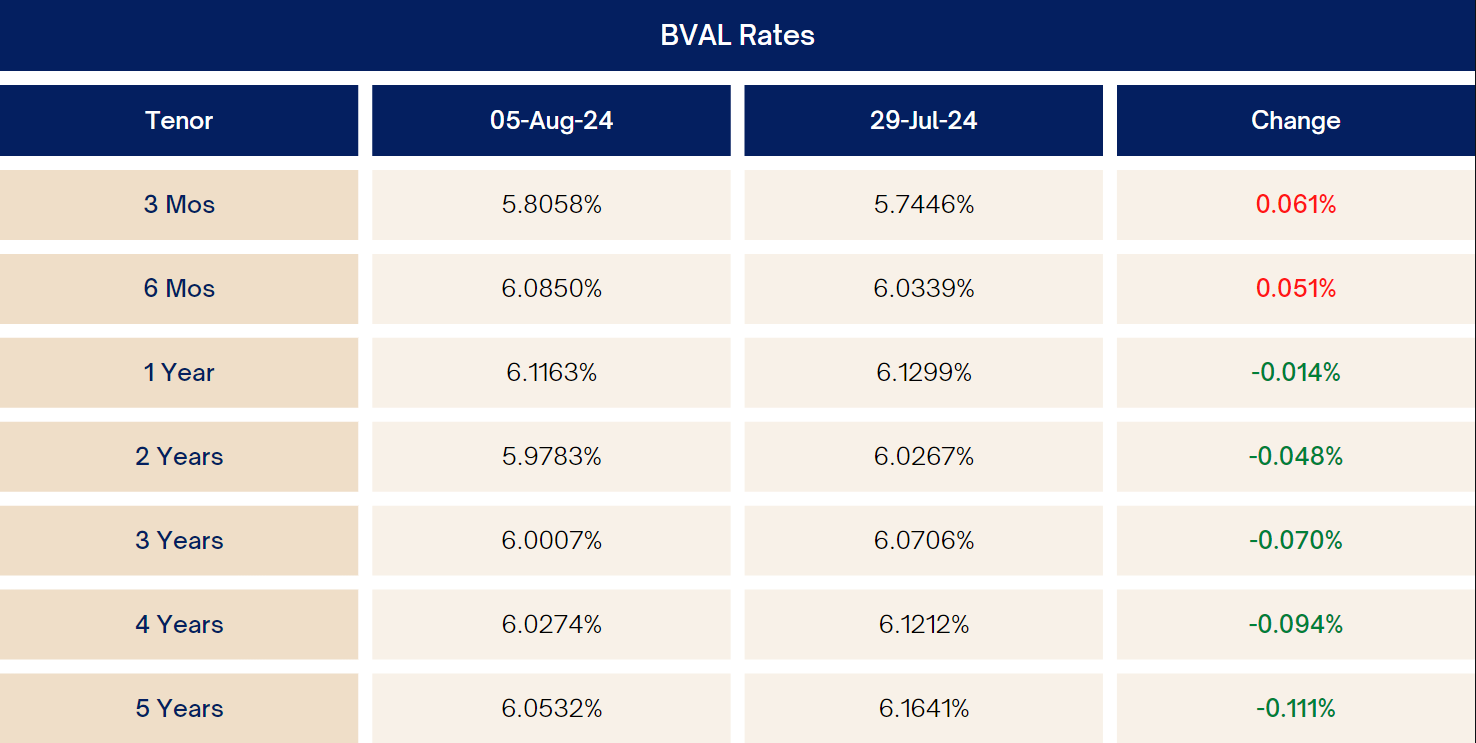

It was a good week for the local space as aggressive risk-taking continued to push local yields 5-15 basis points lower across benchmark tenors week-over-week (WoW). The move mostly followed the rally in the global bond space, with market participants growing more confident and adding positions ahead of the potential start of the easing cycle.

On the auction front, T-bill offerings showed strong demand, with the Bureau of the Treasury (BTr) fully awarding their T-bill offering at rates 3.5 basis points lower than last week’s auction. It also fully awarded the reissuance of 20-14 (3Y) at an average of 6.009% and a high of 6.034%, which was within market expectations. Despite decent demand for the 3Y auction, the GS curve ended flatter, with dealers looking to load up in the 5- to 20-year space.

Towards the end of the week, however, GS lagged behind the continued rally in rates as players looked to take profit on their holdings. Overall, 10-72 and 20-27 ended the week 10bps lower each at 6.150% and 6.295% respectively. Elsewhere, RTB 5-18 continues to be the most traded bond, ending 10.7 basis points lower WoW at 6.115%.

On August 6, the BTr fully awarded the reissuance of 7-67 (5Y) at an average rate of 6.107% and a high of 6.128%, which was in the upper range of market expectations. The GS curve steepened slightly as dealers offloaded in the 10- to 20-year space, given the higher-than-expected inflation release of 4.4% compared to the 4.1% consensus.

Market Levels (week-on-week)

WHAT WE CAN EXPECT

At current levels, the desk suggests starting to take profit on bonds in the back-end, given how narrow they are against bonds in the belly of the curve, and to reposition through the BTr’s upcoming auctions.

See our top picks below:

Note: Rates are indicative and subject to refresh.