DOWNLOAD

DOWNLOAD

Peso GS Weekly: Anticipated rate cut spurs activity

We still prefer 5- to 7-year bonds as they continue to provide the most decent term-premium across the curve.

By Metrobank Local Currency Trading Department and Maria Christina Virtudazo

By Metrobank Local Currency Trading Department and Maria Christina Virtudazo

WHAT HAPPENED LAST WEEK

Better selling interest in the peso government securities (GS) was seen to start last week as players de-risked ahead of the 20-year supply, with most bonds trading 4 basis points (bps) higher. Given the flat shape of the local GS curve and the market still absorbing the additional supply of 10-year bonds from the previous week, participants continued to be better sellers towards the first half of the week.

In last Wednesday’s reissuance of the 20-Year benchmark Fixed Rate Treasury Note (FXTN) 20-27, the Bureau of the Treasury (BTr) fully awarded the reissuance within market indications at an average of 6.43% and a high of 6.47%. Auction participation was relatively subdued compared to the previous two issuances, as the bid-to-cover ratio only reached 1.8x despite the smaller supply.

Good two-way interest was seen for short-dated bonds as sellers freeing up liquidity to fund their awards were met by opportunistic buyers. The inclement weather caused by Typhoon Carina eventually stalled any moves and most dealers were just seen managing client flows.

As the market re-opened, sizable mappings of FXTN 20-27 were seen near the 6.40% area on suspected end-user interest. Buying momentum eventually spilled over to other parts of the curve as 5- and 10-Y bonds traded at 6.22%, and 6.25%, respectively. Overall, most yields ended 1-2bps higher WoW.

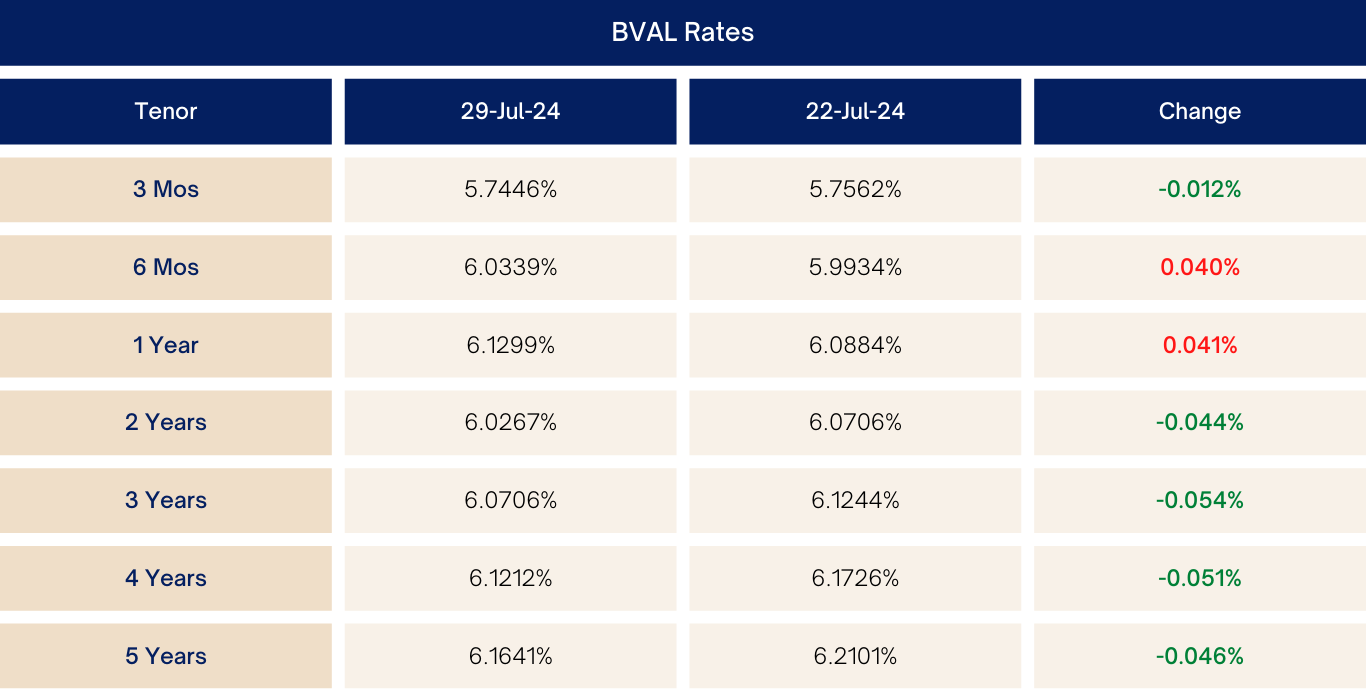

Market Levels (week-on-week)

WHAT WE CAN EXPECT

All eyes will now be on today’s 3-Year FXTN 20-14 reissuance where the desk’s indicative range now stands at 5.95-6.10%. Interested clients are still advised to bid at the higher-end of market indications to close the gap against 5Y bonds.

At current levels, the desk still better prefers 5-7Y bonds as they continue to provide the most decent term-premium across the curve. Clients who are looking to deploy in the 12-15Y space may wait for better levels before reinstating positions given how flat the curve is. Elsewhere, the BTr just released their borrowing plan for 2025, which shows PHP 2.04 trillion planned domestic borrowing, coming from the PHP 1.93 trillion this year.

See our top picks below:

Note: Rates are indicative and subject to refresh.