DOWNLOAD

DOWNLOAD

Peso GS Weekly: Buy the belly, sell the back-end

Participants show better buying interest in medium-term bonds, while some took profit on long-dated bonds.

By Metrobank Local Currency Trading Department and Maria Christina Virtudazo

By Metrobank Local Currency Trading Department and Maria Christina Virtudazo

WHAT HAPPENED LAST WEEK

Throughout the week, the local government securities (GS) market experienced varied activity, influenced by global yield movements and upcoming economic data releases. Price action was mostly two-way, with participants biased toward a steepening curve.

Buying interest was more dominant in the belly of the curve, while a mix of profit-taking and bottom-fishing interest was seen in long-dated securities. The back-end of the curve, however, saw less activity as most participants were still inclined to unload.

The most active securities in the belly were the Retail Treasury Bond (RTB) 5-18 and Fixed Rate Treasury Notes (FXTNs) 20-17, 10-69, and 10-72. In the 20-Year part of the curve, interest was seen in FXTNs 20-26 and 20-27, as dealer profit-taking was met by some participants reinstating positions.

Last Tuesday, the Bureau of Treasury (BTr) fully awarded the reissuance of the FXTN 10-72 at an average rate of 5.89%, with accepted bids ranging from 5.873% to 5.895%. After the bond auction, sideways trading was seen with day-on-day movements very limited.

For the remainder of the week, the market took cues from global yield movements, but bonds remained supported as supply was done for the year. On a week-on-week basis, yields traded within a tight 3 to 5 basis points (bps) range from the previous week’s close.

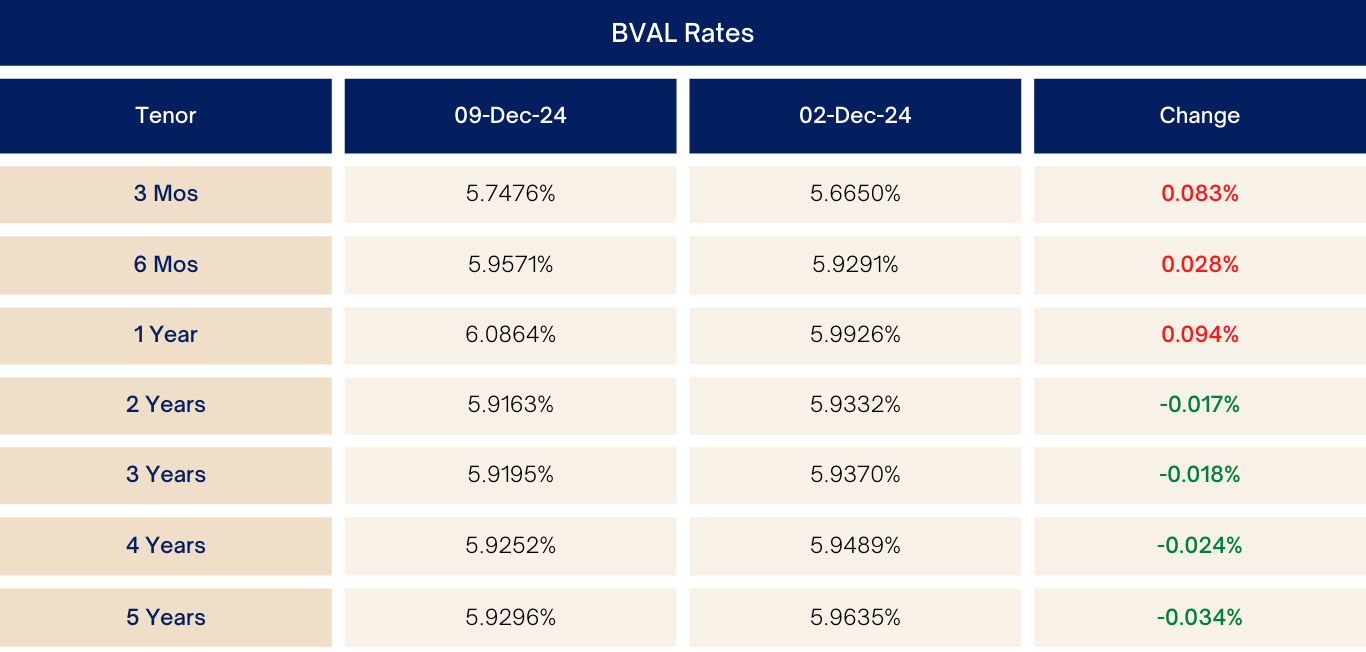

Market Levels (week-on-week)

WHAT WE CAN EXPECT

We caution clients from overloading on bonds in the back-end part of the curve at this time, as we expect bond supply to revert to regular volumes come January. This additional supply pressure should provide opportunities to enter at even better entry levels for end-users.

Those looking to deploy funds may still purchase 2- to 4-Year bonds, as these hold value compared to bonds in the 10- to 20-Year part of the curve that provide little to no yield pick-up.

This week, all eyes will be on the movements of the US Federal Reserve and the Bangko Sentral ng Pilipinas. As of today, both central banks are expected to implement a 25-bp cut to their key policy rates.

Beyond this week’s events, market participants will also be on the lookout for the fourth quarter borrowing program of the BTr where we expect supply to be concentrated in 5- to 20-Year bonds.

See our top picks below:

Note: Rates are indicative and subject to refresh.

(Disclaimer: This is general investment information only and does not constitute an offer or guarantee, with all investment decisions made at your own risk. The bank takes no responsibility for any potential losses.)